Expiration of Moratoriums (and what it means for community associations)

The Federal moratorium on evictions and foreclosures expired July 31, 2021. While this rule was specifically for federally backed mortgages, many other mortgage providers and agencies, including condo/HOA collectors, were honoring this guidance.

Now that the moratorium has expired, what should we expect? There is a fair amount of confusion over the program and the significance of July 31. An article from CNET helps clarify the program and the relevant dates. Here is what we need to understand for community associations:

- There will be an increase in condo/HOA foreclosures in the coming months.

- The majority of the remaining forbearance plans will expire between September 30 – December 31, 2021.

- Owners can still request mortgage forbearance until September 30 that could extend through March 31, 2022.

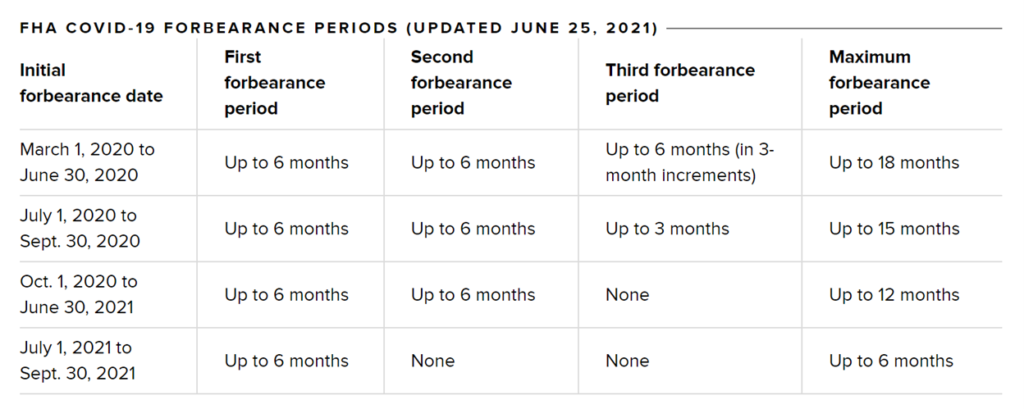

Based on this information, we can surmise that there will be some immediate uptick in activity simply because many non-FHA collectors were honoring the July 31 date. And the trend will continue through March 2022 as the remaining forbearance plans expire. The chart below from the FHA lays out the forbearance periods.

The Washington Post provides a dire perspective, characterizing the deferred debt as a tsunami that is about to hit homeowners. Regardless of whether the impact comes as a tidal wave or a flood, the impact will be felt by communities. Here are the numbers that you and your community need to know:

- Over 2 million homeowners are delinquent on their mortgages

- 8 million are in forbearance

- 5 million are 3+ months behind

- 10% of those in forbearance do not have adequate equity

- 5% of delinquent homeowners are unemployed

- 8% of those in forbearance are using the money to pay other bills

Attom Data sees a concentration of foreclosures in 50 vulnerable counties: “The report reveals that a stretch of states running from Connecticut through Florida, plus Illinois, had 43 of the 50 counties most vulnerable to the economic impact of the pandemic.” Most owners that had the means to get out of forbearance are already back on track, but those still in forbearance are unlikely to get caught up on their mortgage, property taxes, and insurance. And once that reality sets in, we will see an increase in HOA/condo delinquencies. Homeowners facing the reality that they can’t afford to keep their home will keep whatever cash they can and let the debt holders, including their HOA, jockey for position once the home is sold or foreclosed.

Here are some important steps to take for your community:

- Ensure your collection policy is being followed. Many communities slow-rolled collections during the pandemic, but now is the time to be vigilant and consistent.

- File liens to protect your interests if you are not in a state with statutory lien laws for condos & HOAs.

- Use a hardship verification service like the free tool at hardshipcalculator.com when hardship claims or payment terms are requested by a homeowner.

- Make sure your collector does a thorough risk analysis of all delinquencies to screen for bankruptcies, military activity, bank foreclosure, and lien priority.

- Require your collector to use current technology and predictive analytics to maximize ROI and reduce costly legal actions.

Now would also be a good time to circulate an RFP to your current attorney/collector while requesting proposals from other collectors in your area. This will bring transparency and accountability to collections, just like you require for all other vendors. The following best practices are suggested to limit risk and cost exposure while increasing transparency into the collection process:

- Use separate agreements for legal representation versus collections with no requirement to use the same firm for both services.

- Require that legal fees related to collections are deferred and collected from the debtor (not paid by your HOA) so that your community does not have to “finance” this cost.

- If your attorney will not defer their collection fees, create a separate budget line for legal fees and costs related to collections to ensure 100% is being recovered.

- Ask your manager to track and report the time to reach a resolution on each delinquency and maintain a running average on the number if days to resolve delinquencies.

- Use proactive efforts to contact owners and negotiate payment prior to legal action and track the percentage of accounts that are successfully resolved without legal action.

For the moment, we may have dodged a bullet when it comes to the economic impact of COVID-related delinquencies in community association. We should be grateful but ever-vigilant in this season of first-ever experiences. We don’t yet know the extent to which delinquencies will increase, but they will increase. The astute Board and Manager will be sure to be prepared.